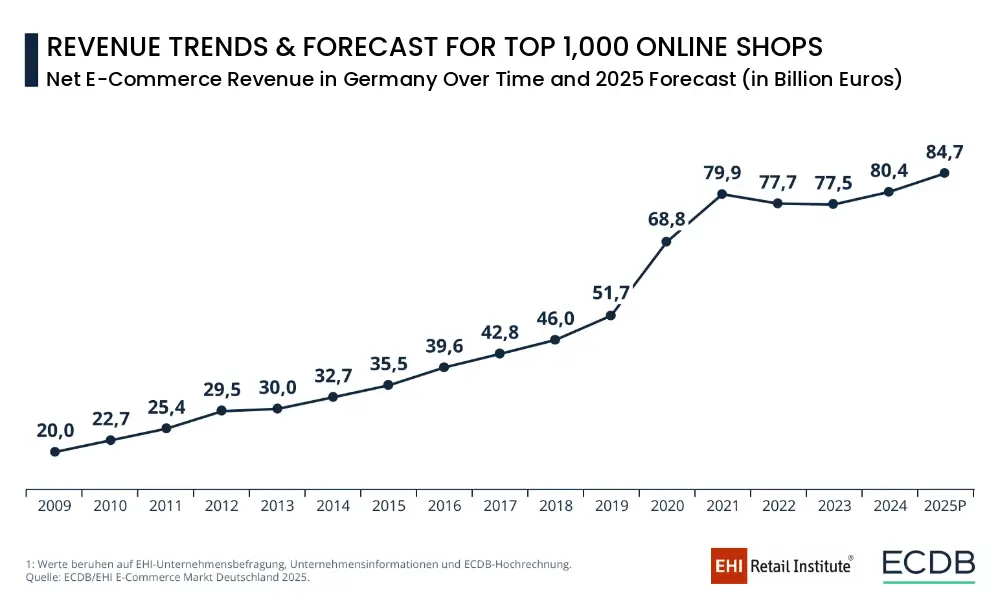

Germany’s online retail sector is gaining momentum, with the top 1,000 B2C online stores achieving notable growth for the first time since 2021. According to the new “E-Commerce Market Germany 2025” study by EHI and ECDB, the net e-commerce revenue of these top retailers increased from €77.5 billion in 2024 to €80.4 billion, reflecting a nominal growth of 3.8 percent or €2.9 billion, and a real growth of 3.0 percent. The report projects a further nominal growth of 5.3 percent for the current year.

Despite the overall market expansion, the report reveals that market growth is heavily concentrated and remains strongly driven by the largest players. Specifically, the ten highest-grossing shops recorded a significant 8.0 percent growth, while the remaining 990 shops saw their revenues increase by only 1.3 percent. This disparity reinforces the dominance of major retailers.

Dr. Friedrich Schwandt, CEO of ECDB, explained the situation: "The market thus remains highly concentrated. Large providers are growing faster and are securing an ever-larger share of the overall market." This trend is clearly reflected in the market share figures: the Top 10 companies now account for 38.8 percent of the total revenue generated by the Top 1,000, while the Top 100 shops generate a commanding 70.7 percent of the overall revenue.

The ranking continues to be dominated by established giants, led by amazon.de (€15.0 billion), followed by otto.de (€4.4 billion), and zalando.de (€2.6 billion). However, the major story of the year involves the top ascenders and the shifting landscape of consumer priorities.

New international players, particularly the China-founded platform shein.com (€1.1 billion / €1.12 billion), have made significant inroads, with Shein entering the Top 10 for the first time at seventh place, ahead of Apple and Ikea. Close behind is shop-apotheke.com (€1.05 billion), which secured eighth place with robust growth of 29.1 percent. The strongest relative growth was posted by rewe.de (€920 million), which showed an impressive 33.5 percent increase, placing it ninth and marking its debut in the Top 10.

EHI e-commerce expert Lars Hofacker noted that "In addition to the established players, providers of daily necessities are increasingly gaining importance." This development is attributed primarily to changing purchasing habits: "Groceries are being ordered online more frequently, for delivery or collection, and the e-prescription is driving digital ordering in pharmacies."

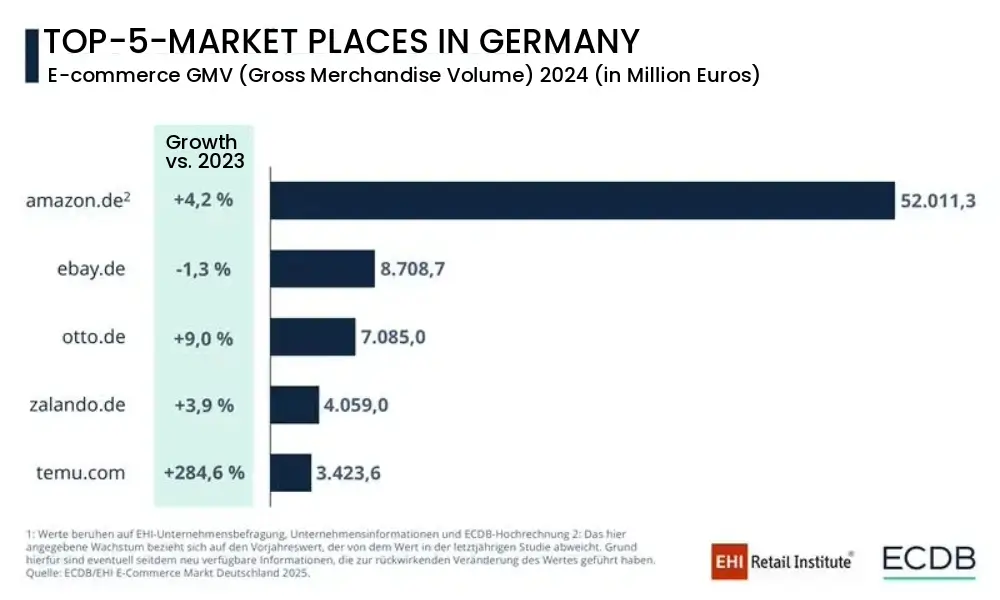

The marketplace segment shows a similar dynamic, with new international competitors rapidly reshaping the structural landscape. While amazon.de, ebay.de, and otto.de maintain their leading positions among B2C marketplaces, otto.de stood out with particularly strong growth in Gross Merchandise Volume (GMV) of 9.0 percent.

The rise of new international platforms is reshaping Germany’s online retail landscape. Temu, a China-based discount marketplace, recorded the strongest growth in relative terms, with revenue nearly tripling to €3.4 billion, achieving 285 percent growth. Temu now ranks fifth among marketplaces, following Amazon, eBay, Otto, and Zalando.

Lars Hofacker explained the significance of this shift, stating: "This clearly shows how quickly new international providers are changing the market structure and challenging established platforms." He added that "The growth of Temu illustrates how intensely competitive pressure is rising in e-commerce, and how dynamically market conditions are shifting."

Shein, selling directly to consumers, ranks seventh overall with €1.12 billion in revenue, just behind Apple and Ikea, but ahead of Shop Apotheke, Rewe, and Aboutyou.

The study also examined payment methods among the top 1,000 online stores, revealing a significant shift towards digital wallets. Apple Pay is now offered by over a third of the stores, marking a 43 percent increase from the previous year, while Google Pay grew by 63 percent, becoming the third most widely available wallet.

PayPal remains the most prevalent, available in 95 percent of online shops. Analysts are closely monitoring emerging payment providers, such as Wero, and their potential impact on the online retail landscape, particularly if integrated with e-commerce platforms.

Overall, Germany’s online retail market shows strong growth and a shifting competitive landscape, driven by both established players and new entrants. With increasing adoption of digital payment solutions and changing consumer habits, analysts expect continued expansion in the sector throughout 2025. The full findings of the “E-Commerce Market Germany 2025” study will be presented at the EHI Connect conference on September 30, 2025, in Düsseldorf and are available for download.

From breaking news to thought-provoking opinion pieces, our newsletter keeps you informed & engaged.

By subscribing, you agree to our Terms & Conditions and Privacy Policy.