Germany's net migration fell to 235,000 in 2025, the lowest figure since 2020 and 45% below 2024. Yet 1.48 million people still arrived. Here is who came, who left, and which countries drove the change.

In 2025, 1,479,944 people moved to Germany while 1,244,944 left, producing net migration of 235,000. That is a 45.4% drop from 430,183 in 2024 and 83.9% below the 2022 peak of 1,462,089. Net migration has fallen every year since 2022,m but the steepest single-year drop was from 2022 to 2023, when the post-invasion Ukrainian wave began to normalise.

.webp)

What's striking isn't just the gap between the gross and the net, it is the volatility itself. Going from +329,000 in 2021 to +1.46 million in 2022 to +235,000 in 2025 is a six-fold swing in four years. No country with a stable, structural migration system produces flows this erratic. Germany's migration is fundamentally event-driven, when a single geopolitical event hits, the national figure swings by close to a million.

The recent decline is driven almost entirely by falling arrivals. Between 2024 and 2025, arrivals dropped by 214,000 (−12.6%) while departures actually fell slightly (−1.5%). Since the 2022 peak, arrivals are down 44.5% while overall departures have changed little. Looking deeper, departures have risen meaningfully in specific groups, Germans, Turks, Syrians, but these are offset by EU departures falling.

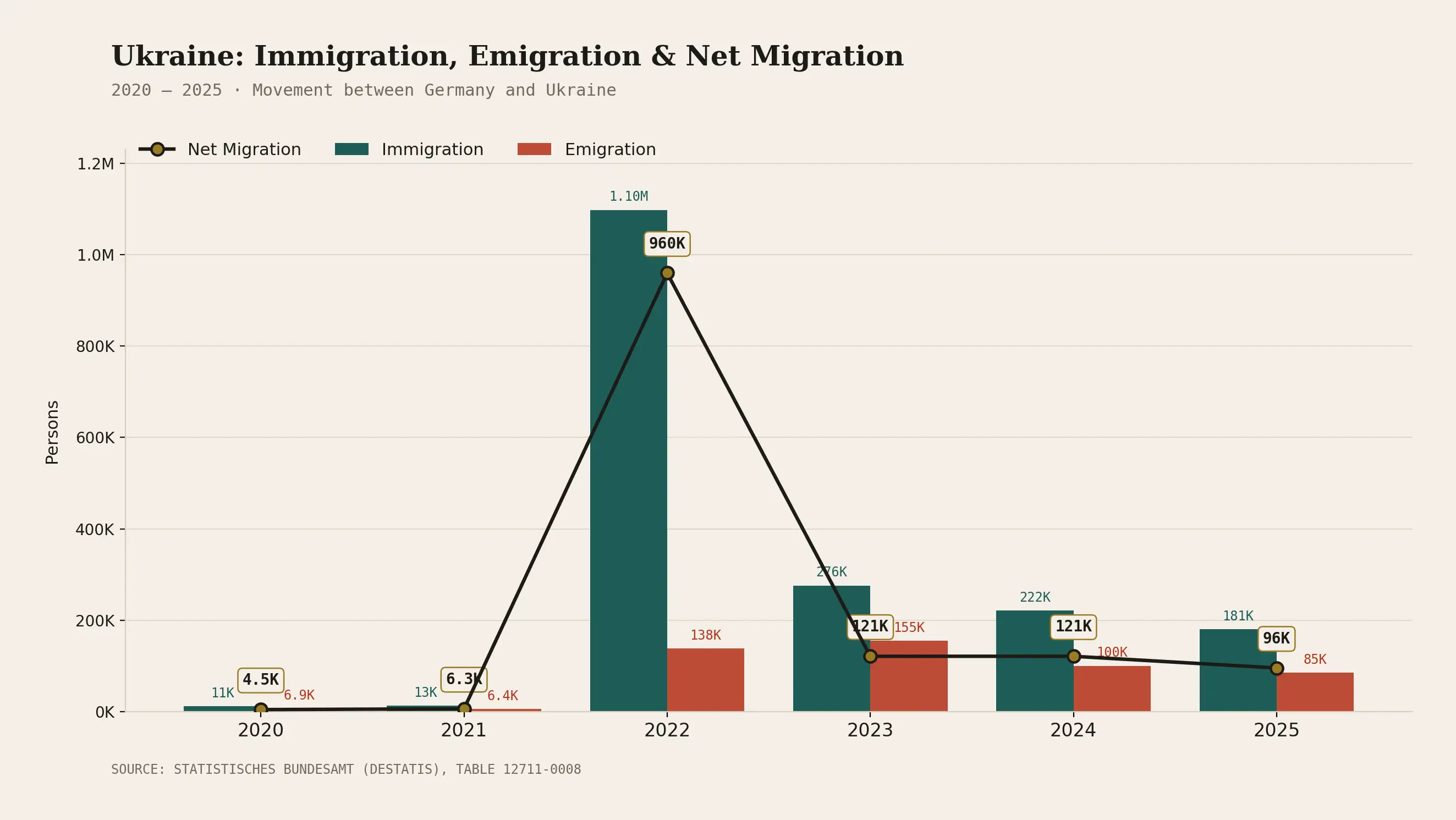

The single biggest factor behind the falling net is Ukraine. After the full-scale invasion in 2022, net migration from Ukraine surged from 6,272 in 2021 to 959,527 in 2022, the largest single-country movement in this dataset by a wide margin. It has fallen every year since, settling at 95,513 in 2025.

Ukraine remains the single largest source of net migration to Germany in 2025. But its decline of 864,014 from the 2022 peak accounts for approximately 70% of the entire 1.2 million drop in Germany's total net migration since then.

This is the clearest evidence of how event-driven Germany's migration has become. Strip Ukraine out of 2022 and the national net would have been roughly 500,000 - high, but recognisable as a continuation of pre-war trends. A single country, in a single year, swung the entire German migration headline by nearly a million. That kind of dependence on one external situation is not normal for a stable migration system.

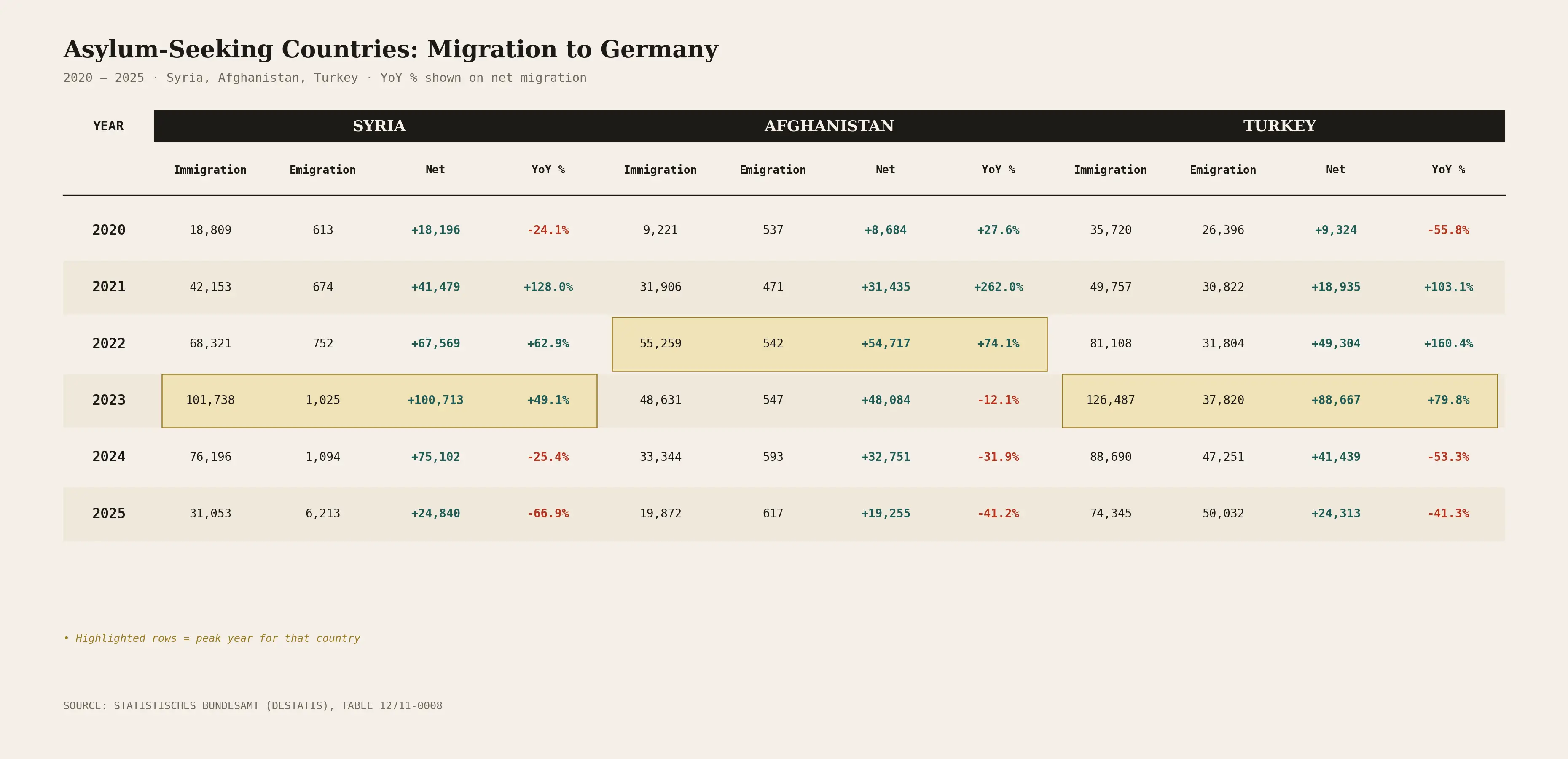

One reason for the lower immigration in 2025 compared to 2024 is a decrease in net immigration from the main countries of origin for asylum seekers. Compared to the previous year, the data records significant declines in net immigration from Syria (−67%, from 75,000 to 25,000), Turkey (−41%, from 41,000 to 24,000), and Afghanistan (−41%, from 33,000 to 19,000).

Looking at the longer arc, all three countries' net migration peaked in different years, Afghanistan at 54,717 in 2022, Syria at 100,713 in 2023, and Turkey at 88,667 in 2023, yet all three are now well below those highs. The asylum-driven wave that defined much of German migration in recent years is unwinding in parallel, regardless of country-specific timing.

A less-discussed but striking shift has emerged among Germany's EU neighbours. Romania, Poland and Bulgaria were strong net contributors as recently as 2022, but all flipped to net negative in 2024 and remained negative in 2025.

Romania went from +35,254 in 2021 to −3,619 in 2025. Poland from +3,787 to −16,870. Bulgaria from +17,591 to −13,744.

The synchronized timing is the most overlooked story in the data. Three countries with very different economies, demographics and migration patterns all flipped to negative in the same year. That kind of simultaneous reversal usually points to a common shock, either Germany's labour market shifted, or conditions at home improved enough to start pulling people back, or both.

What's also notable: in all three cases, the flip was driven by falling arrivals, not rising departures. Romanian, Polish and Bulgarian departures from Germany actually declined from 2022 to 2025. The reversal is about people no longer coming, not people newly leaving.

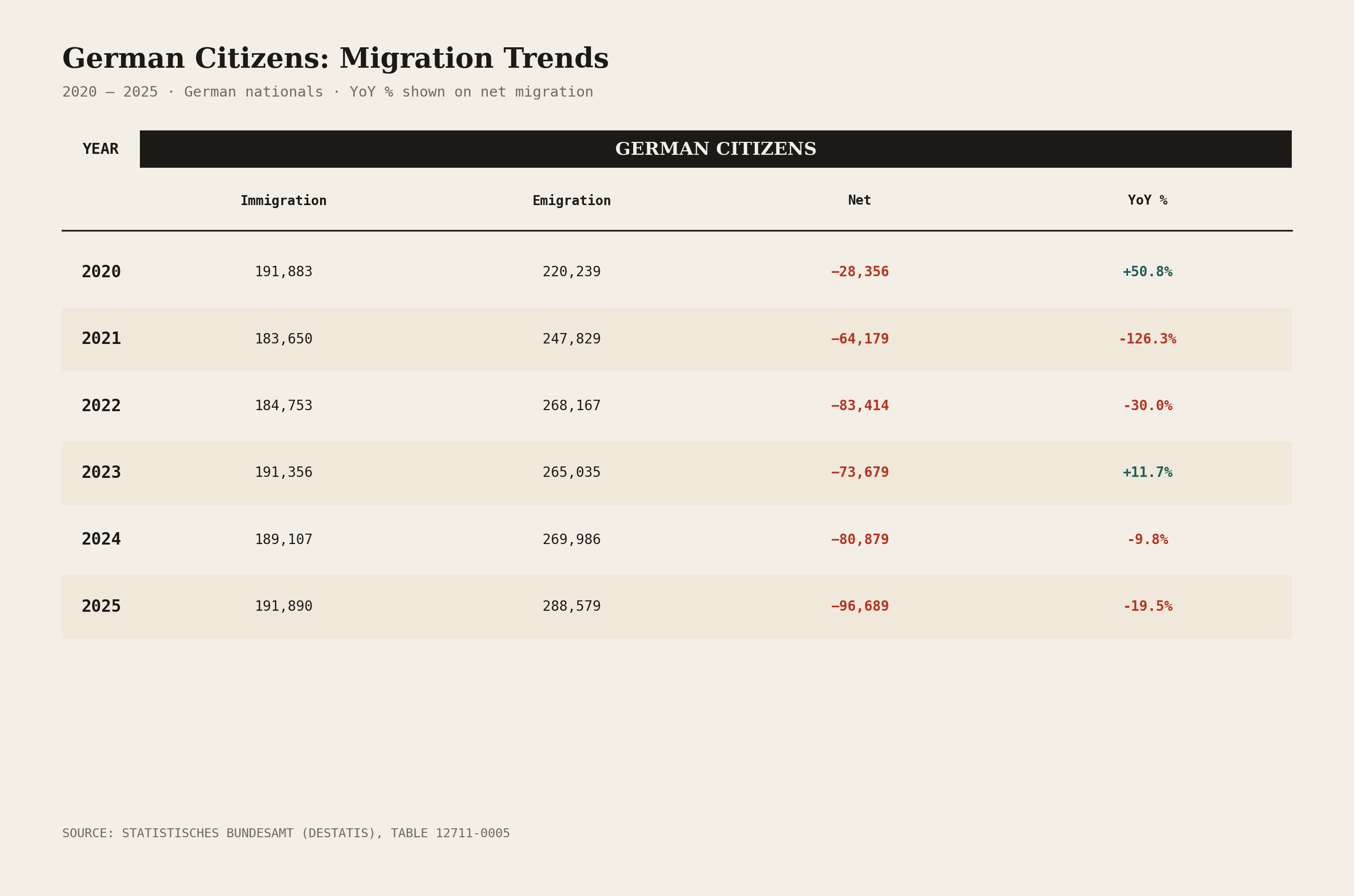

A quiet but persistent trend: more German citizens are leaving than returning. In 2025, 288,579 Germans emigrated while only 191,890 returned, a negative net migration of 96,689 German citizens. The top destinations were Switzerland (22,730 Germans), Austria (13,549), Spain (9,676), the United States (8,860) and France (5,748).

German emigration to Switzerland alone has grown by more than 30% since 2021. But the more important point is the longer arc. The German net loss has widened from −23,528 in 2011, to −57,625 in 2019, to −96,689 in 2025. That's a steady multi-decade drift, Germans choosing to live elsewhere, mostly in richer or sunnier neighbours, in growing numbers every few years.

Each year's number gets dwarfed by foreign inflows and rarely makes headlines, but cumulatively this is the closest thing in the data to a structural trend: Germany has been losing its own citizens, at increasing rates, for fifteen years.

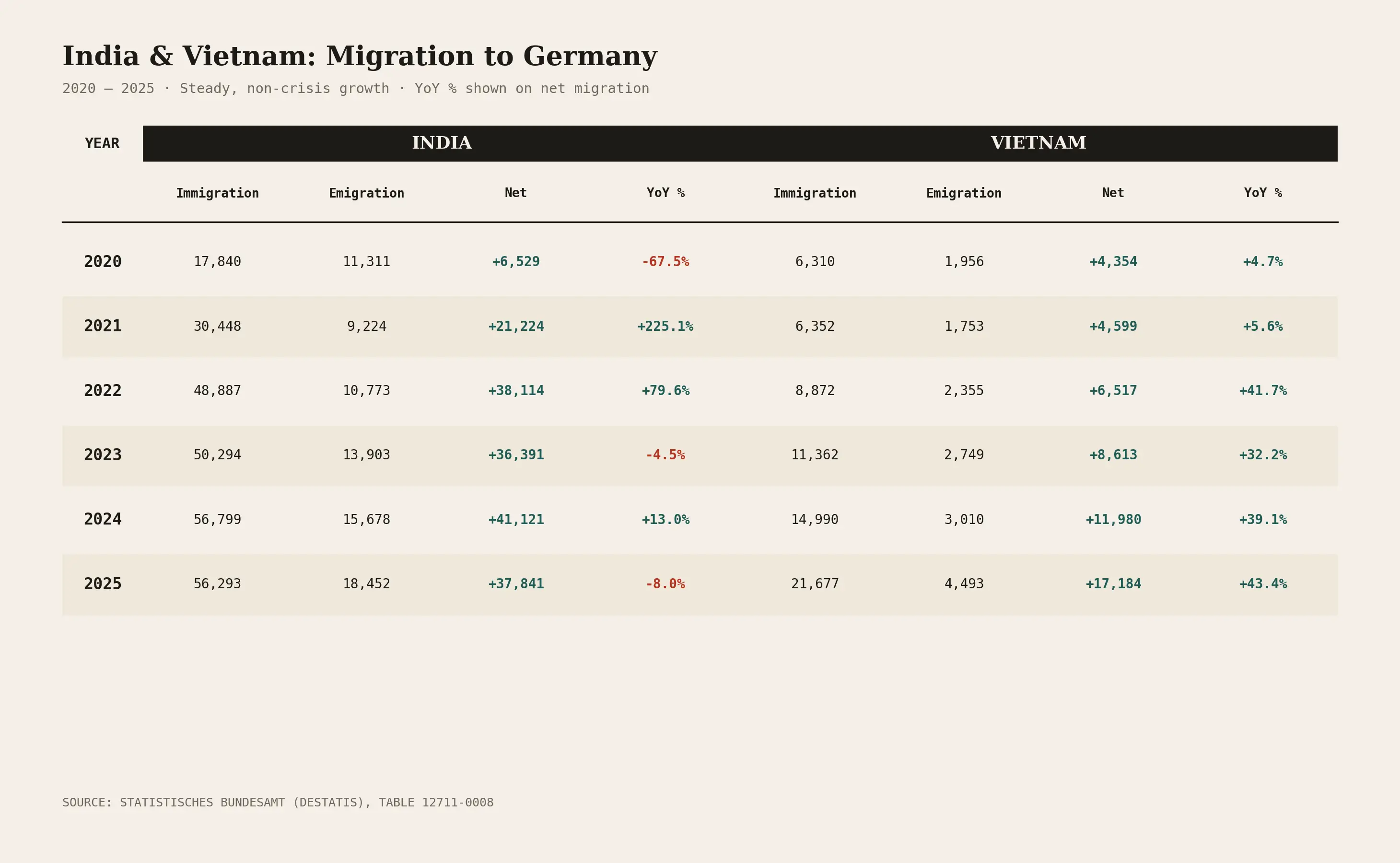

While conflict-driven flows have receded, several Asian countries have shown steady, growing migration without spikes or crisis events behind them. India settled into a stable 36,000–41,000 net range from 2022 onwards, reaching 37,841 in 2025. Vietnam has nearly quadrupled in five years, from 4,599 in 2021 to 17,184 in 2025.

These look like the early-to-middle stages of deepening migration chains, labour agreements, study programmes, family networks compounding on themselves. They are linked to skilled labour and student migration patterns rather than crisis-driven flows. This is the underrated story in German migration. While attention stays on conflict origins, this group is quietly building. These are the slow-moving trends that look small year-to-year but become the structural backbone of a migration system over a decade.

Other Asian countries follow a similar shape but at smaller scale. China contributed a net of 8,176 in 2025 (down from 10,940 in 2024), and the Philippines added 3,615, both showing the same gradual, non-volatile pattern.

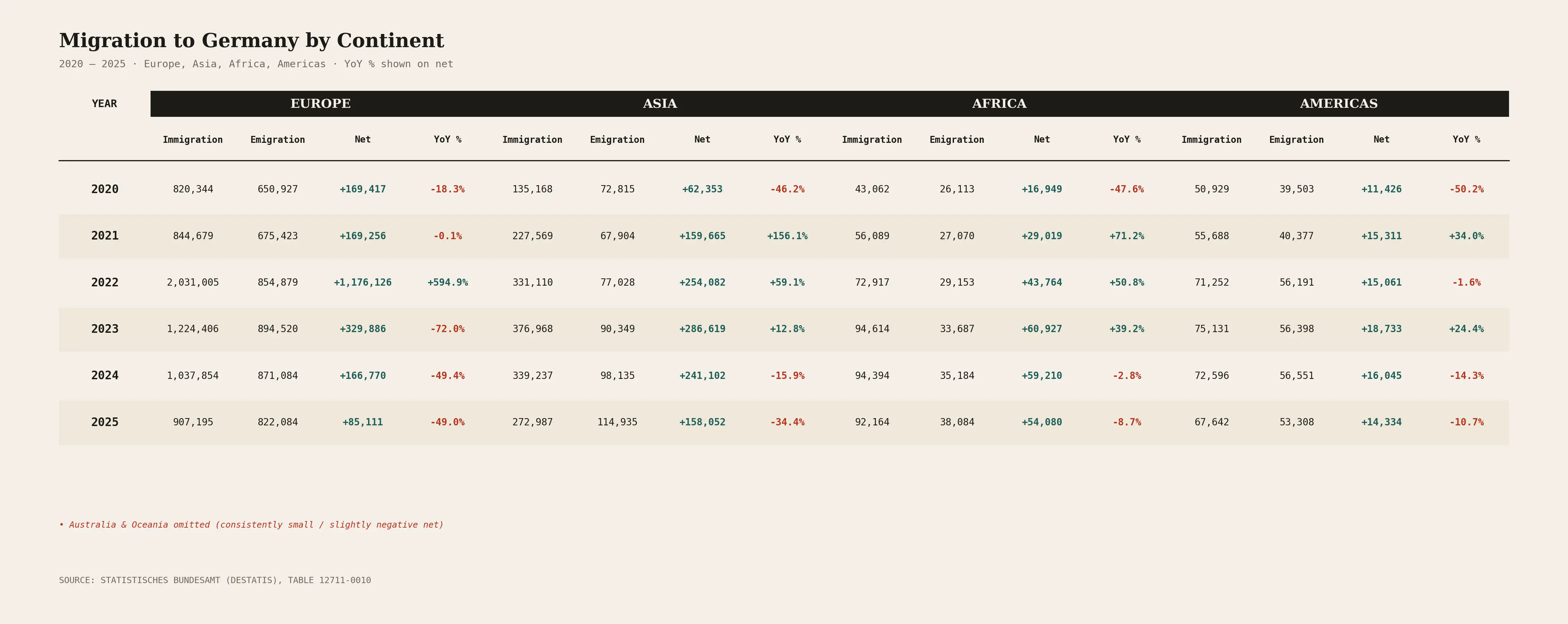

Asia drove the largest net contribution to Germany in 2025 at 158,052, down from 241,102 in 2024. Europe followed at 85,111 (down from 166,770), Africa at 54,080, the Americas at 14,334, and Australia and Oceania at −801.

Every continent's net gain shrank year-on-year, but Asia and Europe took the deepest absolute drops, together they explain the bulk of the national decline. Both happen to be the continents most exposed to the fading conflict flows: Ukraine sits in Europe; Syria, Afghanistan and Turkey are all classified within Asia or its borderlands. When those flows fade, the continent totals follow.

North Rhine-Westphalia drew the most foreign arrivals at 294,337 (down 15.6% from 2024), followed by Bavaria (265,942, down 14.8%), Baden-Württemberg (221,664, down 11.5%), Lower Saxony (144,015), Hesse (134,070) and Berlin (120,392).

Every leading state saw fewer foreign arrivals in 2025 than in 2024, there is no regional outlier resisting the national trend. On net foreign migration, North Rhine-Westphalia added 58,834, Bavaria 42,437, Berlin 40,383 and Baden-Württemberg 39,465. Berlin's number stands out, it has roughly a third of Bavaria's population but a net foreign gain almost as large. The city is absorbing migrants at a much higher rate per capita than the rest of the country.

Across all nationalities, 2,476,160 movements occurred across state borders in 2025, meaning roughly 1 million people relocated between German states internally, on top of international migration. Germany is not just a country migrants enter; internally it is also a country in constant motion.

Perhaps the most striking pattern in the 2025 data: just five countries - Ukraine, India, Syria, Turkey and Afghanistan, account for 86% of Germany's entire net migration. Ukraine alone contributes 40.6% of the total net. Every other nationality combined accounts for the remaining 14%.

This isn't a curiosity, it's a strategic exposure. Germany's effective migration profile depends on five external situations it doesn't control: the war in Ukraine, India's labour relationship with Germany, Syria's reconstruction trajectory, Turkey's domestic conditions, and Afghanistan.

Any meaningful change in any one of these, Ukraine's war ending and Ukrainians returning home, an Indian policy shift, a deeper Syrian stabilisation, could move the German national headline by tens of thousands. That's an enormous amount of external dependency for a country whose demographic future relies on migration.

Germany's 2025 immigration data tells a layered story, and the headline net figure of 235,000 misses most of it. What actually changed is the composition: Ukraine has come off its wartime peak, conflict-origin flows have receded, EU return migration has accelerated in synchronised fashion, and German emigration has continued a fifteen-year structural drift. Five very different stories are happening underneath one number.

Most of these movements are event-driven and reversible. Only one, the quiet growth of Asian skilled migration, looks structural. If that's the case, then in five or ten years Germany's migration headlines may look very different from today. The crisis-driven flows that have dominated discussion for a decade will continue to fade. The slow-building labour and student will keep compounding. And Germany's own emigration trend, which currently nobody is paying enough attention to, has shown no sign of slowing."

The 235,000 net figure is the residual of all this. It is small, fragile, concentrated in a handful of countries, and likely to keep moving with events Germany cannot control.

From breaking news to thought-provoking opinion pieces, our newsletter keeps you informed & engaged.

By subscribing, you agree to our Terms & Conditions and Privacy Policy.